READ TIME: 10 MINUTES

The Internal Revenue Service (IRS) recently released Revenue Procedure 2023-29, reducing the Affordable Care Act’s (ACA) affordability percentage to 8.39% for plan years beginning in 2024, down from 9.12% in 2023 (which was further decreased from 9.61% in 2022).

The affordability percentage is the maximum rate of the employee’s household income that a person can spend on self-only coverage while allowing the employer to comply with the ACA’s affordability requirement.

With the 8.39% 2024 rate, health plans will be priced at their lowest levels since the ACA was passed. With both the Inflation Reduction Act of 2022 and the American Rescue Plan Act of 2021 expanding the ACA premium tax credit subsidies while decreasing the percentage of household income required to be contributed for Marketplace coverage, industry experts expect to see continued reductions to the affordability percentages for years to come.

What does this mean for employers?

- For plan years beginning in 2024, applicable large employers (ALEs) must offer at least one health plan that does not exceed 8.39% of the employee’s household income for the cost of self-only coverage.

- As a reminder, ALEs are employers with an average of 50 or more full-time or full-time equivalent employees in the previous calendar year.

- Because of this rate reduction, ALEs may need to revisit both employer and employee contributions to the health plan to meet the new affordability requirement.

How do employers determine whether their health coverage is affordable under the ACA?

The ACA provides for three “safe harbors” for affordable employer-provided health coverage:

- Federal Poverty Level Safe Harbor

- Rate of Pay Safe Harbor

- W-2 Wages Safe Harbor

If the employer satisfies one of these safe harbors, then their health coverage is affordable under the ACA.

Let’s look at each in turn.

Federal Poverty Level (FPL) Safe Harbor

For 2024 calendar year health plans, the plan will satisfy the FPL safe harbor if a full-time employee pays no more than $101.93 monthly for self-only coverage. (Note that for employees working in Alaska, the rate is $127.31 monthly, and for those working in Hawaii, the rate is $117.25 monthly.) These monthly amounts constitute no more than 8.39% of the federal poverty level, which is determined annually.

Employers should note that for the FPL safe harbor, they are permitted to use the federal poverty guidelines in effect six months before the beginning of the plan year, to provide employers with adequate time to establish premium amounts in advance of the plan’s open enrollment period.

If that six-month look-back period reaches into a prior calendar year, and two FPL affordability safe harbor amounts are available (one for the previous year and one for the current year), the employer can choose between the two amounts when applying the FPL safe harbor.

For example, for a health plan that starts May 1, 2024, the employer may “look-back” to the FPL safe harbor amount applicable for 2023 ($110.81 per month for mainland U.S.) or for 2024 ($101.93 per month for mainland US), choosing to use either in its FPL affordability calculation.

However, if a health plan starts September 1, 2024, looking back six months would only reflect the 2024 FPL safe harbor amount ($101.93 per month for mainland U.S.), which must be used in the employer’s FPL affordability calculation.

If an employer decides to use this look-back approach, the ACA affordability percentage that applies for the year in which the health plan starts must be used. For example, for any health plan starting in 2024, 8.39% applies even if the look-back period enables the employer to use the 2023 FPL amount ($110.81 per month for mainland U.S.).

Rate of Pay Safe Harbor

The rate of pay safe harbor will be satisfied if a full-time employee’s cost for self-only coverage does not exceed 8.39% of their monthly salary (or hourly rate multiplied by 130). This safe harbor uses the lowest monthly salary for salaried full-time employees and the lowest hourly rate of pay for hourly full-time employees to determine affordability.

W-2 Wages Safe Harbor

The W-2 wages safe harbor will be satisfied if a full-time employee’s cost for self-only coverage does not exceed 8.39% of their annual wages, as reported on their Form W-2. This safe harbor can often be more challenging as employers do not always know the exact amount of reported W-2 wages until the end of 2024. Therefore, the other two safe harbors are typically recommended.

With the 2024 ACA affordability percentage now released, employers should begin proactively strategizing with their health plan broker or consultant to meet these new affordability requirements.

What penalties may employers face if they fail to satisfy the ACA’s affordability requirements?

An ALE that does not meet the ACA’s employer mandate and has at least one full-time employee who receives a subsidy when enrolling in Marketplace coverage may face one of two penalties:

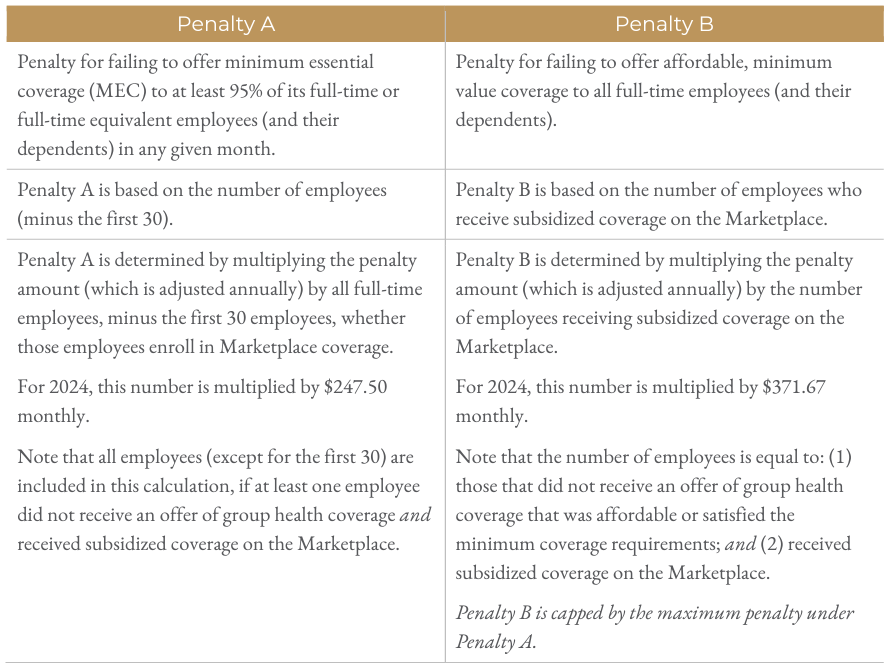

- Penalty A: Penalty A applies to an ALE if that employer fails to offer minimum essential coverage (MEC) to at least 95% of its full-time employees in any given month (or more than five employees if fewer than 100 employees).

This penalty is triggered if at least one full-time employee, who did not receive an offer of MEC, receives a subsidy when enrolling in Marketplace coverage.

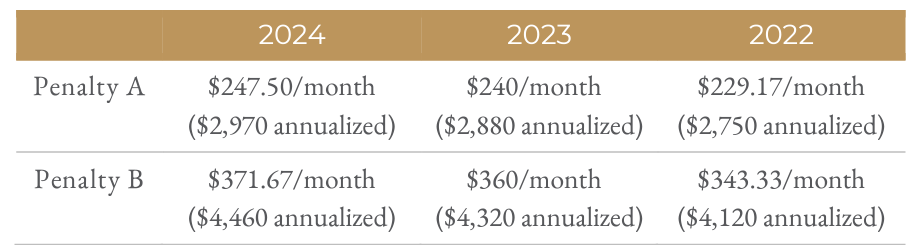

Penalty A is determined by multiplying the penalty amount (adjusted annually) by all full-time employees, minus the first 30 employees, whether those employees enrolled in Marketplace coverage.

- Penalty B: Penalty B applies to an ALE if that employer offers MEC to at least 95% of its full-time employees in any given month but fails to offer affordable, minimum value coverage to all full-time employees.

This penalty is triggered if at least one full-time employee receives a subsidy when enrolling in Marketplace coverage and that employee did not receive coverage that satisfied the affordability or minimum value requirements under the ACA.

Penalty B is determined by multiplying the penalty amount (adjusted annually) by the number of employees receiving subsidized coverage on the Marketplace.

Here’s a glance at the 2024 penalties, compared to both the 2022 and 2023 penalties:

To better understand when each ACA penalty might apply, this table compares Penalty A and Penalty B, based on 2024 penalty amounts.

The IRS has stated that there is no statute of limitations for these ACA penalties.

How does the IRS determine whether an ALE owes a penalty?

When determining whether an ALE owes an ACA penalty, the IRS compares the employer’s ACA reporting with the list of employees who purchased health coverage through the Marketplace and received a subsidy.

If the IRS determines that a penalty is owed, the employer will receive a 226-J Notice Letter from the IRS, outlining the penalty amounts.

Next Steps for Employers

- For plan years beginning in 2024, ALEs must be aware of the reduced ACA affordability rates, taking these lower rates into consideration when designing their health plan contributions.

- As such, ALEs must offer at least one health plan that satisfies one of the affordability safe harbors for employer-provided health plans.

- ALEs may need to revisit their health plan strategy with their broker or consultant to meet the new 2024 affordability requirement.

This information has been prepared for UBA by Fisher & Phillips LLP. It is general information and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors.